{kind=link}

Freelancing gives you freedom — but it also hands you a tax responsibility that no employer manages for you. The good news? Freelancers in India actually have more tax-saving options than salaried employees, and most freelancers don’t use even half of them. In this guide, you’ll learn the best tax-saving options for freelancers in India, with real numbers and a worked example.

When I got my first big freelance payment, I happily spent most of it — and then got a rude shock at tax time when I realized I owed tax on the full amount, plus interest for not paying advance tax. That one mistake cost me nearly ₹12,000 in penalties. Everything in this article is what I wish someone had told me that year.

Do Freelancers Pay Tax in India?

Yes. Freelance income is taxed as “Profits and Gains from Business or Profession”. If your total income exceeds the basic exemption limit, you must pay income tax — and if your tax liability exceeds ₹10,000 a year, you must also pay advance tax in quarterly instalments.

But here’s the freelancer advantage: unlike salaried people, you’re taxed on profit (income minus expenses), not gross income.

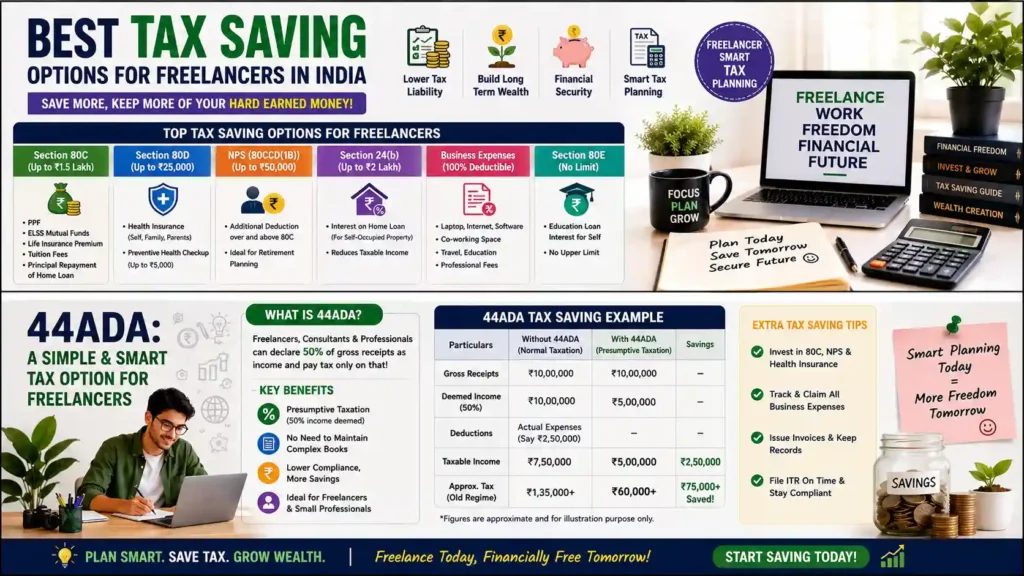

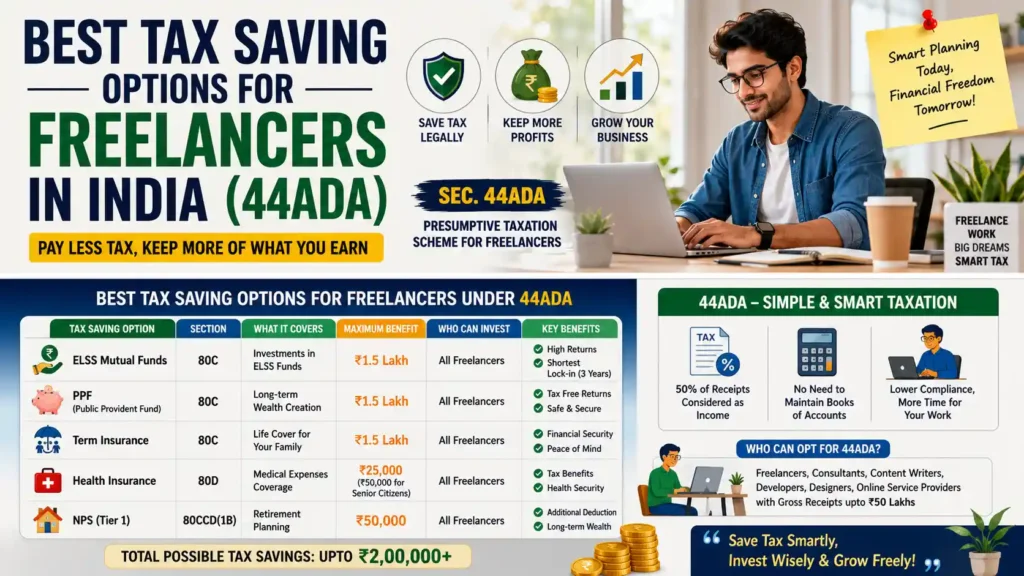

Option 1: Section 44ADA — The Freelancer’s Best Friend

This is the single biggest tax saver for most Indian freelancers.

How it works: Under presumptive taxation (Section 44ADA), you can declare just 50% of your gross receipts as taxable income — no expense proofs, no bookkeeping, no audit (up to ₹75 lakh in receipts if 95%+ payments are digital).

| Gross Freelance Income | Taxable Income under 44ADA |

|---|---|

| ₹10 lakh | ₹5 lakh |

| ₹20 lakh | ₹10 lakh |

| ₹30 lakh | ₹15 lakh |

Who can use it: Professionals like writers, designers, developers, consultants, video editors, and other specified professions.

I switched to 44ADA in my second year of freelancing, and my ITR filing went from a weekend-long headache with expense spreadsheets to about 40 minutes on the income tax portal. For most freelancers earning under ₹75 lakh, it’s a no-brainer.

Option 2: Claim Business Expenses (If Not Using 44ADA)

If your actual expenses are more than 50% of income, skip 44ADA and claim real expenses instead:

- Laptop, phone, camera — as depreciation

- Internet and mobile bills (work portion)

- Rent — proportionate, if you work from home

- Software subscriptions — Adobe, Canva Pro, hosting, domain, AI tools

- Co-working space fees

- Travel for client meetings

- Payments to sub-contractors or assistants

- Courses and upskilling related to your work

Rule of thumb: If expenses > 50% of income → claim actual expenses. If expenses < 50% → use 44ADA.

Option 3: Section 80C — Save Up to ₹46,800 in Tax

Invest up to ₹1.5 lakh per year in these and deduct it from taxable income (old regime):

| Investment | Lock-in | Returns |

|---|---|---|

| ELSS mutual funds | 3 years | Market-linked (~12% avg) |

| PPF | 15 years | ~7.1%, tax-free |

| Life insurance premium | Policy term | Varies |

| 5-year tax-saver FD | 5 years | ~7% |

For most young freelancers, ELSS is the best 80C option — shortest lock-in and highest growth potential.

Option 4: NPS — Extra ₹50,000 Deduction (Section 80CCD(1B))

The National Pension System gives you an additional ₹50,000 deduction over and above 80C. That’s ₹2 lakh in total deductions — worth up to ₹62,400 in tax saved at the 30% slab.

Option 5: Health Insurance — Section 80D

Freelancers have no employer health cover, so this one is both a tax saver and a necessity:

- Up to ₹25,000 deduction for your own family’s premium

- Additional ₹25,000–₹50,000 for parents’ premium (₹50,000 if they’re senior citizens)

Option 6: Choose the Right Tax Regime

- New regime (default): Lower slab rates, but almost no deductions. Zero tax up to ₹12 lakh income (after rebate) in 2026.

- Old regime: Higher rates, but you keep 80C, 80D, NPS, and expense deductions.

Freelancer shortcut: 44ADA works in both regimes. Many freelancers now do best with 44ADA + new regime — declare 50% of income, pay the low new-regime rates, done. Run both calculations (any free online tax calculator works) before filing.

Worked Example: Freelancer Earning ₹15 Lakh

Using 44ADA + new regime (2026 slabs):

| Step | Amount |

|---|---|

| Gross receipts | ₹15,00,000 |

| Taxable income under 44ADA (50%) | ₹7,50,000 |

| Tax under new regime (after rebate) | ₹0 |

Yes — a freelancer earning ₹15 lakh can legally pay zero income tax because 44ADA halves the income to ₹7.5 lakh, which falls under the new regime’s rebate threshold. A salaried person on the same ₹15 lakh would pay ₹1 lakh+.

Don’t Forget: Advance Tax Deadlines

If your yearly tax exceeds ₹10,000, pay advance tax in four instalments: 15 June, 15 September, 15 December, 15 March. Missing these means 1% monthly interest under Sections 234B/234C.

I now keep a separate bank account where I move 15% of every client payment the day it arrives. When advance tax dates come, the money is already sitting there. It’s the single best freelancer money habit I’ve built.

Which ITR Form Should Freelancers File?

- ITR-4 — if using presumptive taxation (44ADA)

- ITR-3 — if claiming actual business expenses

FAQs

Do freelancers pay more tax than salaried employees in India?

Usually less, if they plan well. Section 44ADA alone lets freelancers declare only 50% of income as taxable — a benefit salaried employees don’t get.

Can freelancers claim a laptop as a business expense?

Yes, as depreciation — but only if you’re claiming actual expenses (not under 44ADA, where expenses are already presumed).

Is Section 44ADA good for all freelancers?

It’s excellent if your real expenses are under 50% of income and your receipts are under ₹75 lakh. If your expenses are higher, claim actual expenses via ITR-3 instead.

Do freelancers need to pay GST?

Only if annual turnover exceeds ₹20 lakh (₹10 lakh in some states). Exporting services (foreign clients) can qualify as zero-rated with an LUT.

What happens if a freelancer doesn’t file ITR?

Penalties up to ₹5,000, interest on unpaid tax, and trouble getting loans, visas, or credit cards — ITR is a freelancer’s income proof.

Final Thoughts

The best tax saving options for freelancers in India come down to a simple stack: 44ADA to halve your taxable income, the right regime choice, NPS and 80D where they still help, and disciplined advance tax payments. Set aside 15% of every payment from day one, and tax season becomes a formality instead of a panic.

Also read: [How to Save Money on ₹30,000 Salary in India] and [How to Start SIP with 500 Rupees]

Disclaimer: This article is for educational purposes only. Consult a chartered accountant for advice specific to your situation.”