{kind=link}

Think you need thousands of rupees to start investing? Wrong. In India, you can start a SIP with just ₹500 per month — less than what most of us spend on one food delivery order. In this guide, you will learn exactly how to start a SIP with 500 rupees, which apps to use, which funds are beginner-friendly, and how much your ₹500 can grow over time.

I started my own first SIP with exactly ₹500 in a Nifty 50 index fund back when I was still figuring out my finances. It felt almost embarrassingly small at the time. Today that habit has grown into a monthly SIP of ₹6,000 — but it all started with that first ₹500.

What is a SIP? (Simple Explanation)

SIP stands for Systematic Investment Plan. It means automatically investing a fixed amount (like ₹500) in a mutual fund every month. Think of it like a recurring deposit — but instead of fixed bank interest, your money is invested in the stock market through a mutual fund, which has historically given 10–14% average annual returns over the long term.

Can I Really Start a SIP with Just ₹500?

Yes. Most mutual funds in India accept SIPs starting at ₹500 per month, and many now accept as low as ₹100. SEBI (the market regulator) has been pushing for “micro SIPs” to make investing accessible to everyone.

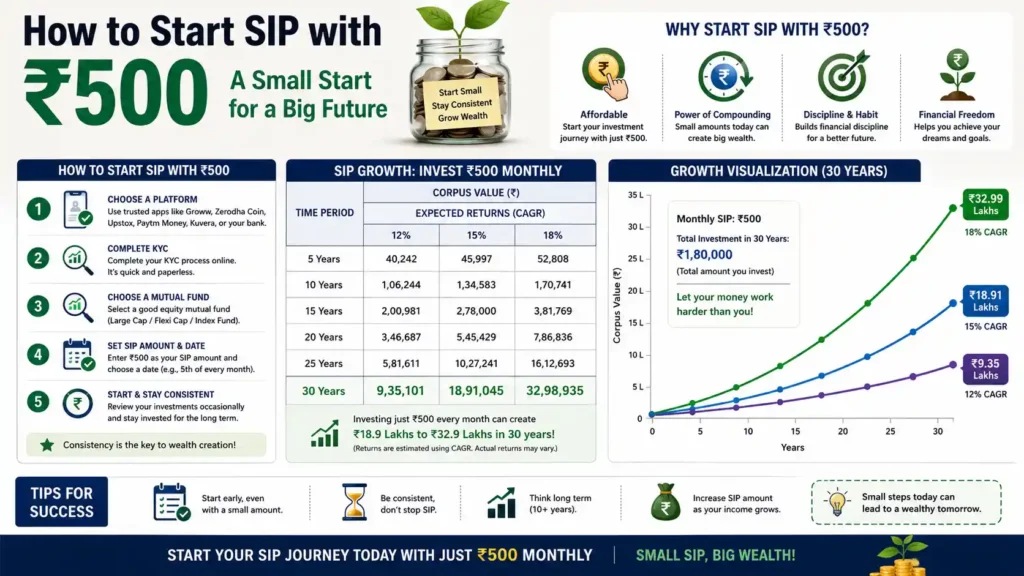

How Much Will ₹500 Per Month Grow? (Real Numbers)

Assuming an average 12% annual return from an index fund:

| Duration | Total Invested | Estimated Value |

|---|---|---|

| 5 years | ₹30,000 | ₹41,000 |

| 10 years | ₹60,000 | ₹1.16 lakh |

| 15 years | ₹90,000 | ₹2.52 lakh |

| 20 years | ₹1.2 lakh | ₹4.99 lakh |

| 30 years | ₹1.8 lakh | ₹17.6 lakh |

Key insight: In 30 years, you invest only ₹1.8 lakh but get back nearly ₹17.6 lakh. That is the power of compounding — and why starting early matters more than starting big.

Step-by-Step: How to Start SIP with 500 Rupees

Step 1: Keep These Documents Ready

- PAN card

- Aadhaar card (linked to your mobile number)

- Bank account with net banking or UPI

- A selfie/photo (for video KYC)

Step 2: Choose an Investment App

I personally use Groww for my SIPs because the interface was the least confusing for me as a beginner. My cousin swears by Kuvera. Honestly, the app matters far less than actually starting — I wasted three weeks “comparing apps” before realizing they all do the same thing.

Popular free apps in India that allow ₹500 SIPs in direct plans (no commission):

| App | Best For

|—–|—–|—–

| Groww | Beginners, simple interface

| Zerodha Coin | Existing Zerodha users

| Kuvera | 100% free, goal-based investing

| Paytm Money | Paytm users

| AMC apps (e.g. Nippon, SBI MF) | Investing directly with the fund house

Important: Always choose a Direct Plan, not a Regular Plan. Direct plans have no commission, which means roughly 1% higher returns every year — a huge difference over 20 years.

Step 3: Complete Your KYC (10 Minutes, Fully Online)

- Download the app and sign up with your mobile number

- Enter PAN and Aadhaar details

- Complete a short video verification

- KYC is usually approved within 24–48 hours

Step 4: Pick a Beginner-Friendly Fund

For a first ₹500 SIP, keep it simple with an index fund:

- Nifty 50 Index Fund — invests in India’s top 50 companies (safest equity option for beginners)

- Nifty Next 50 Index Fund — slightly higher risk, higher growth potential

- Flexi Cap Fund — if you want a fund manager to pick stocks for you

Avoid: sectoral funds, thematic funds, and small-cap funds as your first SIP. They are too volatile for beginners.

Step 5: Set Up the SIP

- Search the fund name in your app

- Select “Start SIP” and enter ₹500

- Choose a date — pick the 2nd or 3rd of the month (right after salary day)

- Set up auto-pay (UPI autopay or bank mandate)

- Done. The money now invests itself every month

5 Golden Rules for Your First SIP

During one market dip, my portfolio was down 14% and I nearly stopped my SIP in panic. I’m glad I didn’t — within a year, those “cheap” units bought during the fall became my best-performing investment. Now I actually look forward to red days.

- Do not stop the SIP when markets fall. Falling markets mean you buy more units cheaply — this is where real wealth is made.

- Increase the amount yearly. Move from ₹500 to ₹1,000 when your salary grows. This is called a step-up SIP.

- Stay invested for 7+ years minimum. Equity works best over long periods.

- Do not check the app daily. Monthly or quarterly is enough.

- Do not chase “top performing” funds. Last year’s winner is often next year’s loser. A boring index fund beats most people’s stock picks.

Is ₹500 SIP Worth It? (Honest Answer)

₹500 alone will not make you rich — but it does three powerful things:

- Builds the habit of investing before spending

- Teaches you how markets move, with money you can afford

- Starts your compounding clock — the earlier you start, the more time your money has to grow

Most successful investors started small. The person who starts a ₹500 SIP at age 22 usually ends up wealthier than the person who waits until 30 to start a ₹5,000 SIP.

FAQs

Can I start a SIP with 500 rupees per month?

Yes. Most mutual funds in India accept SIPs from ₹500 per month, and some allow as low as ₹100.

Which is the best SIP for ₹500 per month?

For beginners, a Nifty 50 index fund (direct plan) is the most recommended option — low cost, diversified, and no fund-manager risk.

Can I withdraw my SIP money anytime?

Yes, mutual funds (except ELSS tax-saver funds, which lock for 3 years) can be withdrawn anytime. Money reaches your bank in 2–4 working days.

Is SIP safe?

SIPs in mutual funds are regulated by SEBI. Market values fluctuate in the short term, but over 10+ years, equity SIPs have historically beaten FDs, gold, and inflation.

Can students or housewives start a ₹500 SIP?

Yes — anyone with a PAN card and a bank account can invest. There is no income requirement.

What happens if I miss a SIP payment?

Nothing serious. There is no penalty from the fund house; your SIP simply skips that month. (Your bank may charge a small mandate-bounce fee.)

Final Thoughts

If you’re a student or just starting your career, please don’t wait like I did. I delayed investing by two years thinking I’d start “when I earn more.” Those two lost years of compounding will cost me more than any bad fund choice ever could.

Starting a SIP with 500 rupees is the single easiest first step into investing. You do not need a demat account, market knowledge, or a big salary — just 10 minutes and a PAN card. Open an app like Groww or Kuvera today, complete your KYC, and set up a ₹500 SIP in a Nifty 50 index fund. Your future self will thank you.

Also read: [How to Save Money on ₹30,000 Salary in India (2026 Complete Guide)]